Categories

Moving to Phoenix?By Scott Bryant | Bryant Luxury Group | Phoenix, AZ

There’s a lot of discussion right now about using Fannie Mae and Freddie Mac to lower mortgage payments.

Buy mortgage bonds.

Cut guarantee fees.

Expand assumable loans.

Offer longer mortgage terms.

On paper, it sounds like relief is coming.

But if you’re buying a home in Phoenix, here’s what matters:

These tools affect financing.

They don’t create inventory.

And inventory is the real pressure point.

They buy loans.

They package loans.

They guarantee loans.

They make borrowing more stable and more available.

But they do not build homes.

They are demand-side mechanisms.

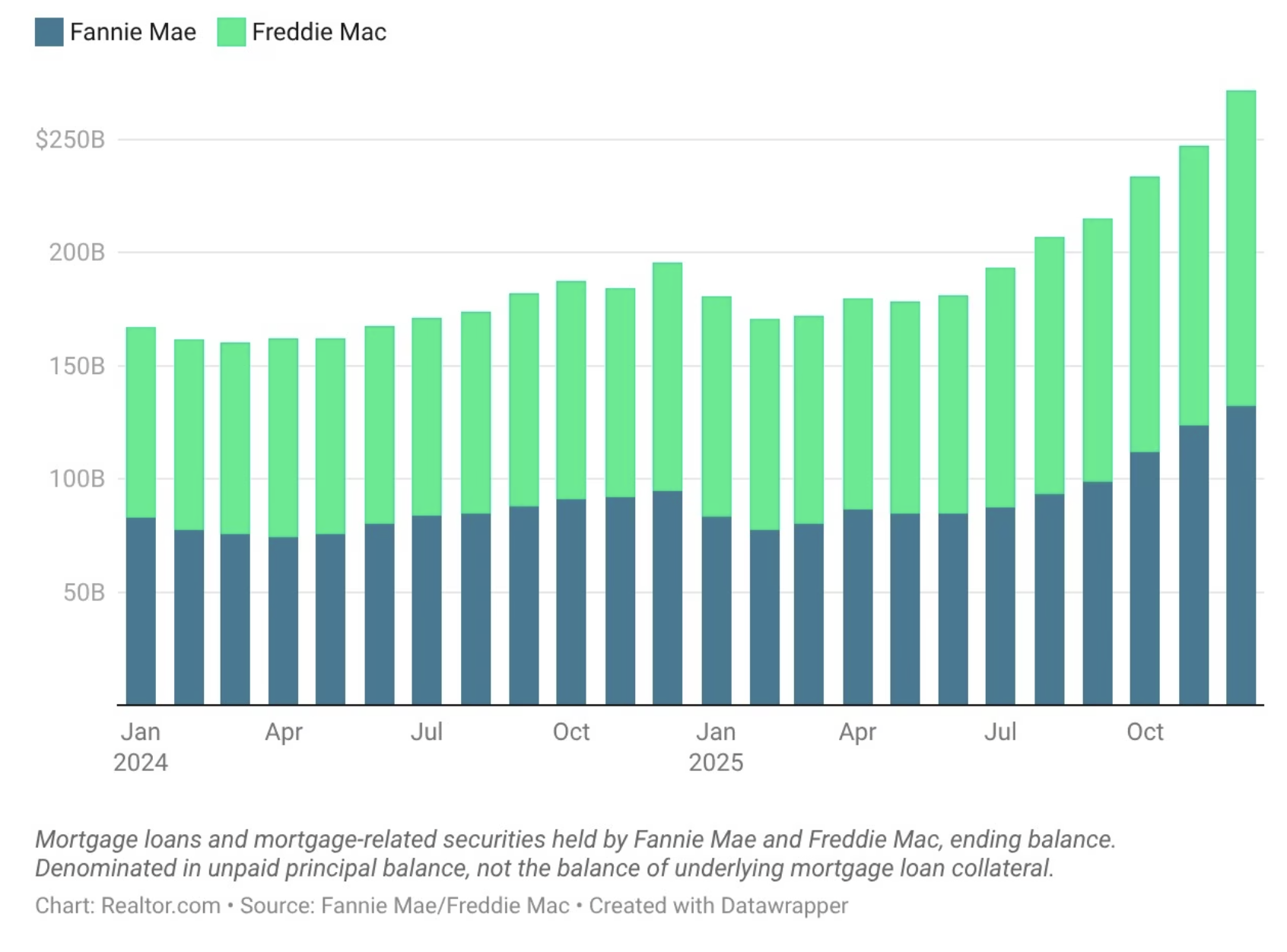

Place the graph immediately after this section.

Use it to visually show how dominant Fannie and Freddie are in the mortgage market. The takeaway for readers should be:

Even though these agencies control a massive portion of U.S. mortgages, their power is concentrated on financing, not housing supply.

We have a supply imbalance.

When demand is steady and supply is tight, prices remain elevated, even if rates drop slightly.

If federal action lowers rates by 0.10%–0.25%, that may reduce a monthly payment modestly.

But if inventory remains constrained, prices absorb that benefit quickly.

Lower rates without more homes often mean:

More competition.

More multiple offers.

Less negotiating leverage.

That’s not theory.

We’ve lived it.

But here’s what buyers need to understand:

Longer loans typically carry higher interest rates.

When you stretch the term and raise the rate, the payment savings shrink dramatically.

In many scenarios, you’re paying almost the same monthly amount, just for 20 additional years.

That’s not affordability.

That’s duration.

In theory, it sounds incredible.

In reality:

It’s a headline-friendly idea with limited practical application.

Federal macro policy moves slowly.

Market structure moves today.

But they do not fix supply constraints.

And Phoenix pricing is primarily influenced by:

Population growth

Available inventory

Construction pace

Buyer competition in specific price bands

If you're buying under $600,000 in North Phoenix, Moon Valley, Desert Ridge, or Central Phoenix, your advantage won’t come from waiting for Washington.

It will come from strategy.

Exactly what to focus on:

✔ Identify motivated sellers

✔ Negotiate concessions aggressively

✔ Understand true monthly payment structure

✔ Avoid emotional bidding in tight pockets

Affordability today is engineered through structure, not speculation.

If you want to see how small rate changes compare to negotiated concessions on a real Phoenix property, I’ll show you both scenarios side by side so you can see what actually impacts your bottom line.

That’s where clarity lives.

—

Scott Bryant

Bryant Luxury Group

Phoenix, Arizona

There’s a lot of discussion right now about using Fannie Mae and Freddie Mac to lower mortgage payments.

Buy mortgage bonds.

Cut guarantee fees.

Expand assumable loans.

Offer longer mortgage terms.

On paper, it sounds like relief is coming.

But if you’re buying a home in Phoenix, here’s what matters:

These tools affect financing.

They don’t create inventory.

And inventory is the real pressure point.

What Fannie and Freddie Actually Do

Fannie Mae and Freddie Mac exist to provide liquidity to the mortgage market.They buy loans.

They package loans.

They guarantee loans.

They make borrowing more stable and more available.

But they do not build homes.

They are demand-side mechanisms.

Place the graph immediately after this section.

Use it to visually show how dominant Fannie and Freddie are in the mortgage market. The takeaway for readers should be:

Even though these agencies control a massive portion of U.S. mortgages, their power is concentrated on financing, not housing supply.

Why That Matters in Phoenix

Phoenix doesn’t have a financing crisis.We have a supply imbalance.

When demand is steady and supply is tight, prices remain elevated, even if rates drop slightly.

If federal action lowers rates by 0.10%–0.25%, that may reduce a monthly payment modestly.

But if inventory remains constrained, prices absorb that benefit quickly.

Lower rates without more homes often mean:

More competition.

More multiple offers.

Less negotiating leverage.

That’s not theory.

We’ve lived it.

The 50-Year Mortgage Conversation

Longer-term mortgages are often pitched as a way to lower payments.But here’s what buyers need to understand:

Longer loans typically carry higher interest rates.

When you stretch the term and raise the rate, the payment savings shrink dramatically.

In many scenarios, you’re paying almost the same monthly amount, just for 20 additional years.

That’s not affordability.

That’s duration.

Assumable Mortgages: Sounds Powerful, Rarely Used

There’s also discussion about expanding assumable loans, allowing buyers to take over a seller’s low rate.In theory, it sounds incredible.

In reality:

- It would apply mostly to future loans.

- It takes years to build usable inventory.

- Even today, FHA loans are assumable, and almost nobody uses that feature.

It’s a headline-friendly idea with limited practical application.

What Actually Helps Phoenix Buyers Right Now

If affordability is the goal, here’s what moves the needle locally:- Seller concessions to buy down rates

- Closing cost credits

- Targeting listings sitting 30+ days

- Negotiating repairs into price adjustments

- Structuring 2-1 buydowns strategically

Federal macro policy moves slowly.

Market structure moves today.

The Bottom Line for Phoenix Buyers

Mortgage policy changes can influence margins.But they do not fix supply constraints.

And Phoenix pricing is primarily influenced by:

Population growth

Available inventory

Construction pace

Buyer competition in specific price bands

If you're buying under $600,000 in North Phoenix, Moon Valley, Desert Ridge, or Central Phoenix, your advantage won’t come from waiting for Washington.

It will come from strategy.

Exactly what to focus on:

✔ Identify motivated sellers

✔ Negotiate concessions aggressively

✔ Understand true monthly payment structure

✔ Avoid emotional bidding in tight pockets

Affordability today is engineered through structure, not speculation.

If you want to see how small rate changes compare to negotiated concessions on a real Phoenix property, I’ll show you both scenarios side by side so you can see what actually impacts your bottom line.

That’s where clarity lives.

—

Scott Bryant

Bryant Luxury Group

Phoenix, Arizona